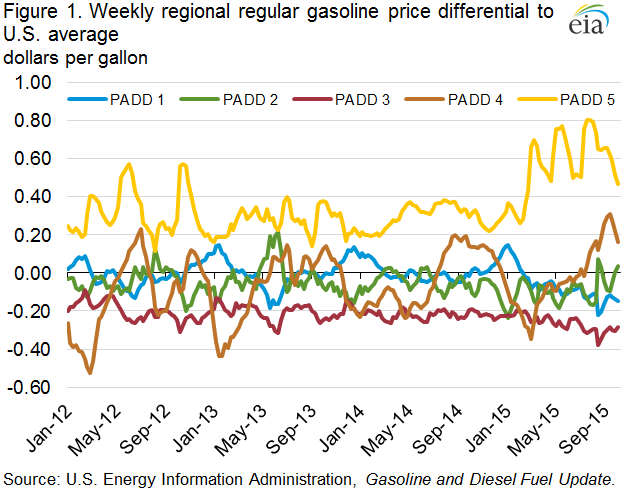

Effects of unplanned refinery outages on prices vary by region

Unplanned refinery outages can have noticeable effects on liquid fuel markets, disrupting supplies of gasoline and distillate. In late August, unplanned outages occurred at two refineries on the East Coast, Petroleum Administration for Defense District (PADD) 1, affecting a significant portion of PADD 1 gasoline production capacity. However, unlike similar incidents on the West Coast (PADD 5) and in the Midwest (PADD 2), there was no significant movement in gasoline prices as a result of the outages. How a region is supplied, what alternative supply options exist, and the costs and lead times for those options will largely determine to what extent prices react to unplanned outages (Figure 1).

While refineries make arrangements for alternative sources of supply during periods of planned maintenance to ensure that obligations are met, it sometimes takes days or weeks for markets to adjust to the sudden loss of production when an unexpected outage occurs. As a result, unplanned refinery outages often result in a reduction in supply that causes prices to increase, sometimes dramatically. The severity and duration of these price spikes depend on how quickly the refinery problem can be resolved and how soon supply from alternative sources can reach the affected market.

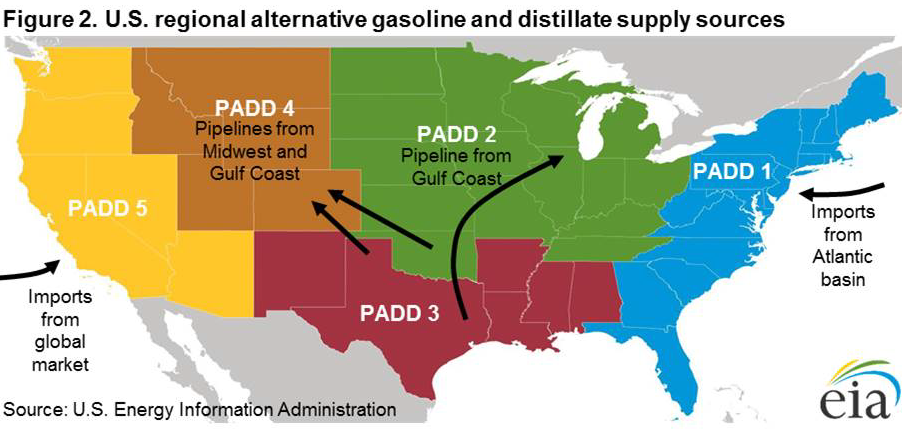

All five PADDs have two immediate sources of alternative supply: inventories and production from other in-region refineries. However, should these sources prove insufficient, the next option for alternative supplies is somewhat different for each region (Figure 2).

The West Coast is isolated from other U.S. markets and located far from international sources of supply, so the region is dependent on in-region production to meet demand. Mainland PADD 5 has three distinct supply/demand centers (Pacific Northwest, Northern California, and Southern California), separated from each other by a lack of north-south pipelines within the PADD and from other U.S. markets by mountains to the east. In the event of a major unplanned refinery outage — such as the one that occurred atExxonMobil’s refinery in Torrance, California in February — inventories and production from unaffected refineries in the immediate area are insufficient to meet demand. Limited pipeline connectivity between market centers and neighboring regions, as well as the more stringent product specifications for California, mean that the only remaining alternative resupply option for PADD 5 is imports.

Since the Torrance outage, imported supplies of gasoline have been arriving in Southern California from all over the world at an average rate of 27,000 — 68,000 barrels per day (b/d) for March through July (latest state-specific data available). This compares with an average of 5,000 b/d in 2013-14. Total motor gasoline imports into PADD 5 as a whole were 79,000 b/d for the week ending October 9. The distance required for these imports requires long lead time and higher prices.

The Rocky Mountain (PADD 4) region is another relatively isolated regional market, but one that still has access via pipelines to refineries in the Gulf Coast and the southern half of PADD 2. Additionally, demand in the Rocky Mountains is small compared to other U.S. markets. Together, these factors allow the Rocky Mountain region to rely on in-region refinery production and receipts from other regions in the event of an unplanned outage.

The Midwest is a large region consisting of multiple semiconnected markets, but without access to international markets via marine movements. PADD 2 refineries produce significant amounts of gasoline and the region has increasingly become dependent on in-region production, but the region still requires additional supplies from the Gulf Coast (PADD 3) to meet demand. In the event of a major unplanned outage, such as the August partial shutdown of the BP refinery in Whiting, Indiana, alternative supply comes from the Gulf Coast via several large product pipeline systems. Although this resupply option requires less time than acquiring supplies from the international market, it does require higher prices in the affected market versus the Gulf Coast to attract supplies, as happened in the summer of 2013 and in early August of this year.

The Gulf Coast is home to half of U.S. refining capacity and produces far more gasoline and distillate than the region consumes. Therefore, unplanned refinery outages in PADD 3 rarely have a large effect on wholesale and retail prices.

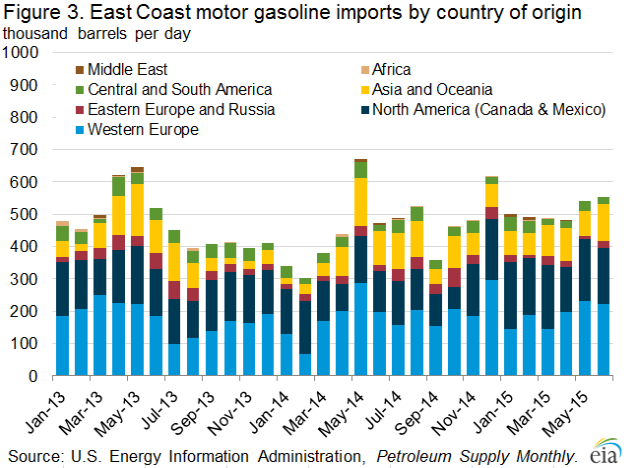

Gasoline demand on the East Coast far exceeds in-region refinery production. Additional supplies from the Gulf Coast arrive via pipeline and ship, but given existing infrastructure and regulations, are not entirely sufficient to meet demand. Therefore, the East Coast also imports gasoline, mostly from relatively close-by refineries in Europe and eastern Canada (Figure 2). In the event of major unplanned refinery outages — like those that occurred at PBF’s refinery in Delaware City, Delaware and the Phillips 66 refinery in Bayway, New Jersey, in late August — the East Coast’s alternative supply option is imports. Because gasoline cargoes are actively traded in the Atlantic Basin, and the distances involved are not as great as on the West Coast, East Coast prices tend to rise more modestly following refinery outages compared with those on the West Coast.

EIA will soon release its Refinery Outages: Fourth-Quarter 2015 report, with data on planned refinery maintenance for the remainder of this year.

U.S. average gasoline and diesel fuel prices increase

The U.S. average regular gasoline retail price increased two cents from the previous week to $2.34 per gallon on October 12, 2015, 87 cents per gallon lower than at the same time last year. The Rocky Mountain and West Coast prices both decreased, by five cents and four cents respectively, to $2.42 per gallon and $2.75 per gallon, respectively. The Midwest price increased five cents to $2.41 per gallon. The East Coast and Gulf Coast prices both increased two cents, to $2.19 per gallon and $2.05 per gallon, respectively.

The U.S. average diesel fuel price increased six cents from last week to $2.56 per gallon, down $1.14 per gallon from the same time last year. The Midwest price increased 15 cents to $2.63 per gallon, supported by widespread refinery maintenance and harvest demand. The West Coast price increased four cents to $2.73 per gallon, while the East Coast price was up three cents to $2.55 per gallon. The Gulf Coast and Rocky Mountain prices each increased two cents, to $2.34 per gallon and $2.52 per gallon, respectively.

Propane inventories gain

U.S. propane stocks increased by 1.8 million barrels last week to 102.2 million barrels as of October 9, 2015, 20.8 million barrels (25.5%) higher than a year ago. Midwest inventories increased by 0.7 million barrels while Gulf Coast and East Coast inventories both increased by 0.6 million barrels. Rocky Mountain/West Coast inventories decreased by 0.1 million barrels. Propylene non-fuel-use inventories represented 4.3% of total propane inventories.

Residential heating oil price increases while propane price decreases

As of October 12, 2015, residential heating oil prices averaged $2.44 per gallon, 2 cents per gallon higher than last week and $1.08 lower than one year ago. The average wholesale heating oil price this week is $1.70 per gallon, nearly 7 cents more than last week and 97 cents per gallon less than a year ago during the same week of the 2014-2015 heating season. Residential propane prices averaged $1.91 per gallon, nearly 7 cents per gallon lower than last week’s price and 46 cents lower than one year ago. Wholesale propane prices averaged nearly 59 cents per gallon, almost 3 cents per gallon higher than last week’s price and 53 cents lower than the price on October 13, 2014.

For questions about This Week in Petroleum, contact the EIA.gov Petroleum Markets Team